SWOT analysis of DMart is more than a management framework. It explains how India’s most admired value retail chain went from a single outlet in Mumbai in 2002 to over 415 stores by FY25, generating revenues above ₹57,000 crore and a market cap crossing ₹2.6 lakh crore.

DMart’s model is built on three cornerstones — everyday low pricing, ownership of real estate to control costs, and ruthless efficiency in working capital. This formula gives the company an edge over competitors like Reliance Retail, BigBasket, Spencer’s and the new wave of quick-commerce players.

What makes this story compelling is not just financial success but the operational discipline behind it. With inventory cycles as short as 31 days and sales per square foot touching nearly ₹34,000 annually, DMart has set benchmarks for modern retail in India.

But the landscape is shifting. Quick-commerce apps are redefining convenience, Reliance is scaling aggressively, and consumers are demanding both price and experience. To stay on top, DMart needs more than low prices — it needs sharper strategy, omni-channel integration, and customer engagement that goes beyond the store walls.

Written by Deepak Singh, Founder of The DM School — Google Partner, 1 Lakh+ students trained, ₹100 Crore+ in client revenue managed. Our experience in digital marketing, funnels, and retail growth gives us a practical lens to decode strategies like DMart’s.

That’s why studying DMart’s SWOT in 2025 is so powerful. It reveals how the company defends its moat, where it’s vulnerable, and what opportunities lie ahead as India’s organised retail sector expands from just 12–18% share of the market. For businesses aiming to capture similar growth online, our SEO company in India shows how visibility and compounding traffic can be engineered with the same discipline.

Quick Answer: DMart’s moat lies in everyday low pricing, owned real estate, and high inventory turns that competitors struggle to match.

Contents

About DMart

DMart is owned and operated by Avenue Supermarts Ltd, founded by billionaire investor Radhakishan Damani in 2002. What started as a single store in Mumbai has grown into a retail powerhouse with more than 415 outlets across India by FY25, spanning over 17 million square feet of retail space.

The company’s strategy has always been simple yet powerful: deliver everyday essentials at prices consistently lower than MRP, backed by efficient supply chain management and cost control. This focus has earned DMart the reputation of being the “Walmart of India.”

Its product mix covers three main categories — Foods (fresh and packaged), Non-Food FMCG (personal care, home care, beverages), and General Merchandise & Apparel. This balance keeps the business resilient, with food driving consistent footfall while discretionary categories add margin potential.

DMart’s presence is strongest in western and southern India, with rapid expansion now happening in the north. The chain has also built its online arm, DMart Ready, which contributed over ₹3,500 crore in FY25. For a business that depends heavily on geographic visibility, mapping and discoverability are critical. That’s where Local SEO services in India mirror the offline principle — ensuring that when customers search nearby, the store shows up first.

Financially, DMart delivered revenues of ₹57,790 crore in FY25 with a profit of nearly ₹2,927 crore. Its inventory cycle of just 31 days and sales per square foot of ~₹34,000 per year are industry-leading benchmarks, making it one of the most efficient retailers in Asia.

Strengths of DMart

Strengths define what DMart does better than anyone else in India’s retail space. These core advantages explain why the company continues to dominate despite new entrants and shifting consumer habits.

1. Everyday Low Pricing (EDLP) – DMart has built its entire brand on value. Products are consistently priced lower than MRP, a strategy made possible by scale, efficient procurement, and owned real estate that minimizes rental costs.

2. Real Estate Advantage – Unlike competitors who lease space at high rentals, DMart largely owns or controls its store properties through long-term agreements. This structure locks in costs, boosts profitability, and provides long-term stability.

3. High Inventory Turns – With an inventory cycle of around 31 days, DMart keeps its capital free-flowing. This ensures shelves are always stocked while keeping working capital tight — a rare balance in Indian retail.

4. Family-Centric Shopping Experience – DMart is positioned as a one-stop destination for Indian households. From rice and atta to cookware and apparel, the brand has designed its stores to cater to an entire family’s shopping list in a single trip.

5. Strong Vendor Relations – Decades of transparent dealings and bulk commitments give DMart bargaining power with suppliers. This ensures consistent supply and better margins compared to smaller chains.

6. Growing Digital Footprint – Through DMart Ready, the chain allows customers to order online and pick up from stores or get doorstep delivery. This hybrid approach blends offline strength with online convenience.

7. Mass Awareness – Unlike smaller retail brands, DMart has become a household name across India. Building such awareness requires consistent branding and reach — something even digital-first companies now strive for. For businesses aiming to achieve this kind of mass brand recall, a YouTube marketing company in India can replicate the formula of high-visibility campaigns at scale.

8. Distribution Network – DMart’s cluster-based expansion strategy ensures that each region has efficient logistics hubs. This keeps supply chains short and reliable, enabling faster replenishment and lower costs.

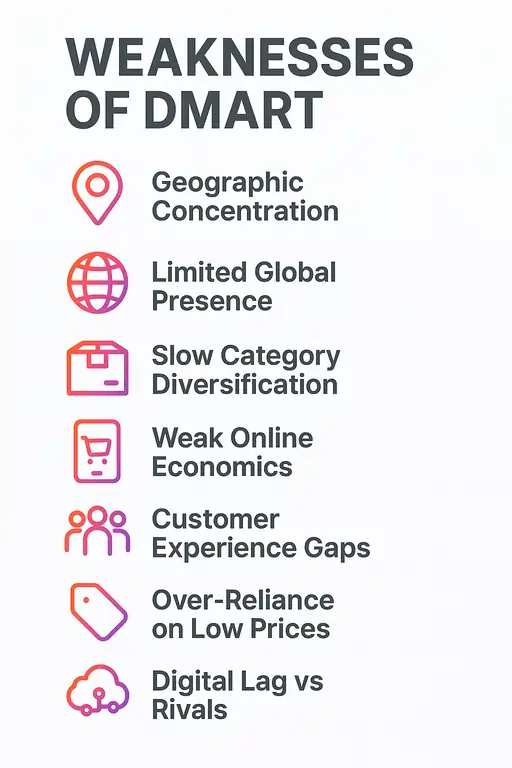

Weaknesses of DMart

Even with its strong moat, DMart is not without vulnerabilities. Identifying weaknesses is crucial because they highlight blind spots that competitors can exploit.

1. Geographic Concentration – Most DMart stores are still clustered in western and southern India. Northern and eastern states remain under-penetrated, leaving huge untapped markets for rivals to capture first.

2. Limited Global Presence – Unlike multinational retailers, DMart is almost entirely dependent on the Indian market. This lack of international diversification makes it more exposed to domestic disruptions and policy changes.

3. Slow Category Diversification – General Merchandise and Apparel (GM&A) still contribute less than pre-Covid levels. While food drives footfall, low GM&A share limits margin growth potential.

4. Weak Online Economics – Though DMart Ready clocked over ₹3,500 crore in FY25 sales, it remains loss-making with a negative EBITDA. Competing with agile quick-commerce models is a constant challenge.

5. Customer Experience Gaps – The no-frills approach keeps costs low but often translates into crowded aisles, long billing queues, and minimal staff training. In today’s retail landscape, experience matters as much as price.

6. Over-Reliance on Low Prices – The brand’s identity revolves around discounts. If suppliers resist aggressive price negotiations or inflation pressures margins, DMart risks eroding its core advantage.

7. Digital Lag Compared to Ecosystem Rivals – Reliance and Tata have integrated retail with payments, telecom, and marketplaces. DMart’s standalone digital play looks limited by comparison, slowing customer lock-in.

For businesses, this highlights a key lesson: being visible across every touchpoint is non-negotiable. If you want to avoid the same blind spot online, explore our Best SEO company in India guide — it shows how to dominate search presence before competitors do.

Opportunities for DMart

Despite challenges, DMart’s growth runway is massive. India’s organised retail penetration is still just 12–18%, leaving wide open spaces to capture. These opportunities can shape the next decade of expansion.

1. North and Tier-II Expansion – DMart has stronghold in western and southern India, but North India remains under-penetrated. Rapid store additions in NCR, UP, and Punjab can unlock millions of new customers.

2. Private Labels – DMart Premia and other in-house brands are just beginning to scale. Increasing private-label share to double digits can boost gross margins by 80–150 basis points, a big lever for profitability.

3. Omni-Channel Advantage – With DMart Ready already contributing ₹3,500+ crore in sales, refining last-mile efficiency and integrating store-attached fulfilment centers can turn it profitable.

4. GM&A Recovery – General Merchandise & Apparel is still below pre-Covid contribution. Reviving this segment with private labels, homeware, and affordable apparel can add both revenue and margins.

5. Quick-Commerce Partnerships – Rather than building its own 10-minute delivery network, DMart could syndicate selected SKUs with Blinkit, Zepto, or Instamart. This hybrid approach secures presence in “need-it-now” baskets without heavy capex.

6. Organised Retail Tailwind – As Indian consumers shift from kiranas to modern retail, DMart stands to win disproportionately thanks to its trusted value-first positioning.

Opportunities aren’t just for giants. Businesses of every size can scale visibility by aligning with consumer shifts. For example, when new stores or private labels launch, high-reach video campaigns deliver awareness at speed. A Best YouTube Ads agency in India can replicate that playbook online — grabbing market share faster than slower-moving competitors.

Threats to DMart

No moat is safe forever. DMart faces multiple external pressures that could impact growth, margins, and market share if not addressed proactively.

1. Quick-Commerce Disruption – Blinkit, Zepto, and Instamart are redefining convenience with under-30-minute deliveries. By 2030, quick-commerce could command over 40% of India’s online grocery segment, eating into DMart Ready’s growth curve.

2. Reliance Retail Aggression – Reliance is scaling Smart Bazaar and JioMart with massive capital, deep supplier tie-ups, and a full ecosystem spanning telecom, payments, and e-commerce. This scale pressure is constant.

3. Persistent Unorganised Retail – Kiranas still dominate ~80% of Indian retail. Their micro-proximity, flexible credit, and personal ties mean DMart cannot fully displace them, especially in smaller towns.

4. Online Price Wars – E-grocery startups often sell at razor-thin margins or even losses to acquire users. This relentless pricing battle threatens DMart’s discount positioning if vendors refuse deeper cuts.

5. Policy and Regulation Risks – Retail is highly sensitive to government decisions — from FDI rules to taxation. Any adverse policy shift can increase costs or slow expansion.

Competition today is no longer limited to store vs. store. It’s a battle of acquisition economics. Businesses that master targeted online funnels will always win more customers at lower cost. If you want to replicate that edge, partner with a Best YouTube Ads agency for lead generation to generate high-quality leads profitably, even in crowded markets.

Competitor Landscape

DMart may be India’s most efficient value retailer, but competition is intensifying from every direction. Understanding these rivals is key to putting DMart’s SWOT into perspective.

Reliance Retail – Through Smart Bazaar, Smart Point, and JioMart, Reliance is the most aggressive player in Indian retail. Its ecosystem play — spanning telecom, payments, and e-commerce — gives it unmatched reach.

Tata Group (BigBasket & Star) – Tata is scaling BigBasket as an omni-channel grocery giant, combining quick-commerce, subscriptions, and doorstep delivery. Star Bazaar adds the offline layer in select metros.

Amazon Fresh – Amazon is pushing convenience-led grocery through its Prime ecosystem. Its strength lies in digital-first customers in Tier-I and Tier-II cities who value convenience over discounts.

Spencer’s & More Retail – While smaller in scale, these chains have strong regional presences. More Retail, in particular, is preparing for expansion and IPO readiness.

Quick-Commerce Startups – Blinkit, Zepto, and Instamart are reshaping customer expectations. Their share of urban grocery is growing fast, particularly among young, convenience-driven consumers.

This battlefield shows how DMart’s moat is tested daily. In the digital world, winning isn’t just about scale but about efficiency of acquisition. For proof, see our YouTube Ads case study — ₹57.58 CPA where we drove 33,500+ conversions at scale with disciplined campaign execution. The same principles apply when competing against aggressive rivals like Reliance or Tata.

How DMart Can Win

Strengths have taken DMart this far, but the future will be decided by strategy. Here are the plays that can keep DMart ahead in 2025 and beyond.

1. Accelerate North India Expansion – Building clusters of 8–12 stores in NCR, Punjab, and UP can replicate the efficiency seen in western markets. This will close the geographic gap with Reliance and Tata.

2. Scale Private Labels – Expanding DMart Premia and other in-house brands into home care, packaged food, and apparel can boost margins by 80–150 bps. This not only defends profitability but builds long-term customer loyalty.

3. Omni-Channel Profitability – DMart Ready must evolve into a hybrid model where store-attached fulfilment centers reduce last-mile costs. Converting online from a loss leader into a profit driver will be a game-changer.

4. Revive General Merchandise & Apparel – GM&A must climb back to pre-Covid contribution levels of 28–29%. Affordable homeware, plastics, and apparel can create stickier baskets and higher margins.

5. Selective Quick-Commerce Tie-Ups – Instead of burning cash to compete head-on, DMart can syndicate fast-moving SKUs on Blinkit or Zepto. This captures “need-it-now” missions without over-investing in logistics.

6. Invest in Experience – Crowded aisles and long queues can hurt brand perception. Better in-store design, staff training, and technology integration can elevate customer experience beyond just low prices.

These plays reflect a simple truth: growth comes from disciplined expansion, margin innovation, and customer-first thinking. It’s the same philosophy that drives our campaigns at Google Partner SEO agency — compounding visibility and scaling ROI in competitive landscapes.

FAQs on SWOT Analysis of DMart

What is the SWOT analysis of DMart?

The SWOT analysis of DMart highlights its strengths like everyday low pricing, weaknesses such as limited online profitability, opportunities in private labels and north India expansion, and threats from Reliance Retail, quick-commerce, and kiranas.

What is DMart’s biggest strength?

DMart’s biggest strength is its everyday low pricing (EDLP) model, enabled by owned real estate and high inventory turns, which allows it to consistently undercut competitors.

What are the weaknesses of DMart?

Key weaknesses include under-penetration in north and east India, a still loss-making e-commerce arm (DMart Ready), and customer experience gaps due to its no-frills approach.

What opportunities lie ahead for DMart?

DMart can expand into northern India, scale private labels like DMart Premia, revive General Merchandise & Apparel, and selectively partner with quick-commerce players to capture faster delivery missions.

What are the threats to DMart?

Threats include Reliance Retail’s aggressive expansion, the rise of quick-commerce players like Blinkit and Zepto, persistent dominance of kiranas, and regulatory changes in the Indian retail sector.

Who are DMart’s main competitors?

DMart competes with Reliance Retail (Smart Bazaar, JioMart), Tata’s BigBasket and Star Bazaar, Amazon Fresh, Spencer’s, More Retail, and fast-growing quick-commerce apps like Blinkit, Zepto, and Instamart.

What is DMart’s future growth potential?

DMart has strong growth potential through cluster-based expansion in new geographies, scaling its private-label portfolio, reviving GM&A contribution, and making its online arm DMart Ready profitable.

Conclusion

DMart is the closest India has to a retail moat. Its disciplined model of everyday low pricing, owned real estate, and efficient operations has delivered unmatched scale and profitability. At the same time, threats from Reliance, Tata, Amazon, and quick-commerce mean the company must evolve beyond just price.

The SWOT analysis shows DMart’s resilience but also its challenges. Opportunities in north India, private labels, and omni-channel integration can define its next phase of growth. Weaknesses like online losses and customer experience gaps need urgent attention.

For marketers and businesses, the lesson is clear: growth comes from compounding visibility and relentless execution. If you want to master the same, explore our resources on Blog Commenting Sites and Directory Submission Sites — proven ways to strengthen authority and drive organic reach.

DMart’s journey proves one point: in a competitive market, the companies that scale with discipline and adapt to change will always lead.